Mark Shore has more than 25 years of experience in the futures markets and managed futures, publishes research, consults on alternative investments and conducts educational workshops (see full biography on page 18).

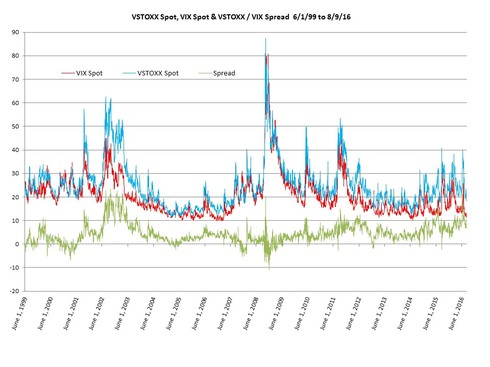

Part 1: Utilizing a European volatility index for Pan-European volatility

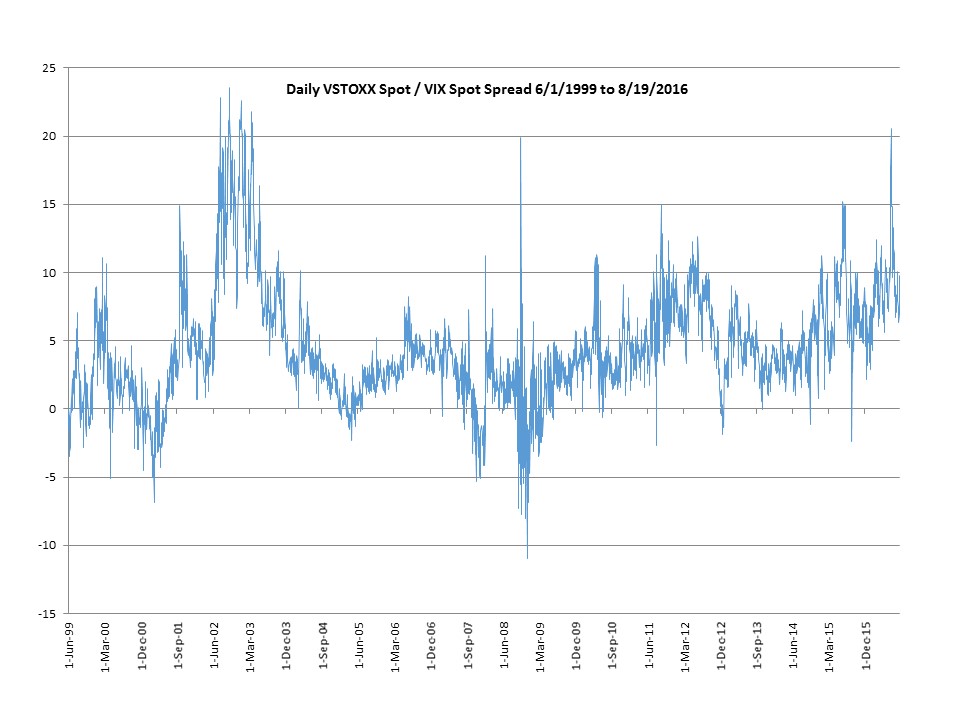

Part 2: VSTOXX®/VIX volatility spread behavior during recent volatility events

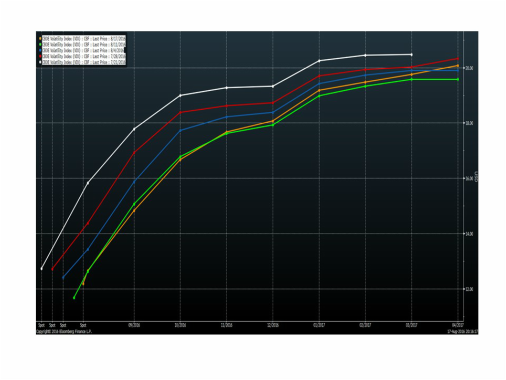

Part 3: Introduction of CFTC-certified options on VSTOXX® Futures

To download the paper click here

Follow Mark Shore on Twitter, Facebook and Linkedin

Copyright ©2017 Mark Shore. Contact Mark Shore for permission for republication at [email protected] Mark Shore has more than 25 years of experience in the futures markets and managed futures, publishes research, consults on alternative investments and conducts educational workshops. www.shorecapmgmt.com

Mark Shore is also an Adjunct Professor at DePaul University’s Kellstadt Graduate School of Business, where he teaches the only known accredited managed futures course in the country. He is also a Board Member of the Arditti Center for Risk Management at DePaul University.

Past performance is not necessarily indicative of future results. There is risk of loss when investing in futures and options. Futures and options can be a volatile and risky investment; only use appropriate risk capital; this investment is not for everyone. The opinions expressed are solely those of the author and are only for educational purposes. Please talk to your financial advisor before making any investment decisions.

Part 1: Utilizing a European volatility index for Pan-European volatility

Part 2: VSTOXX®/VIX volatility spread behavior during recent volatility events

Part 3: Introduction of CFTC-certified options on VSTOXX® Futures

To download the paper click here

Follow Mark Shore on Twitter, Facebook and Linkedin

Copyright ©2017 Mark Shore. Contact Mark Shore for permission for republication at [email protected] Mark Shore has more than 25 years of experience in the futures markets and managed futures, publishes research, consults on alternative investments and conducts educational workshops. www.shorecapmgmt.com

Mark Shore is also an Adjunct Professor at DePaul University’s Kellstadt Graduate School of Business, where he teaches the only known accredited managed futures course in the country. He is also a Board Member of the Arditti Center for Risk Management at DePaul University.

Past performance is not necessarily indicative of future results. There is risk of loss when investing in futures and options. Futures and options can be a volatile and risky investment; only use appropriate risk capital; this investment is not for everyone. The opinions expressed are solely those of the author and are only for educational purposes. Please talk to your financial advisor before making any investment decisions.

RSS Feed

RSS Feed